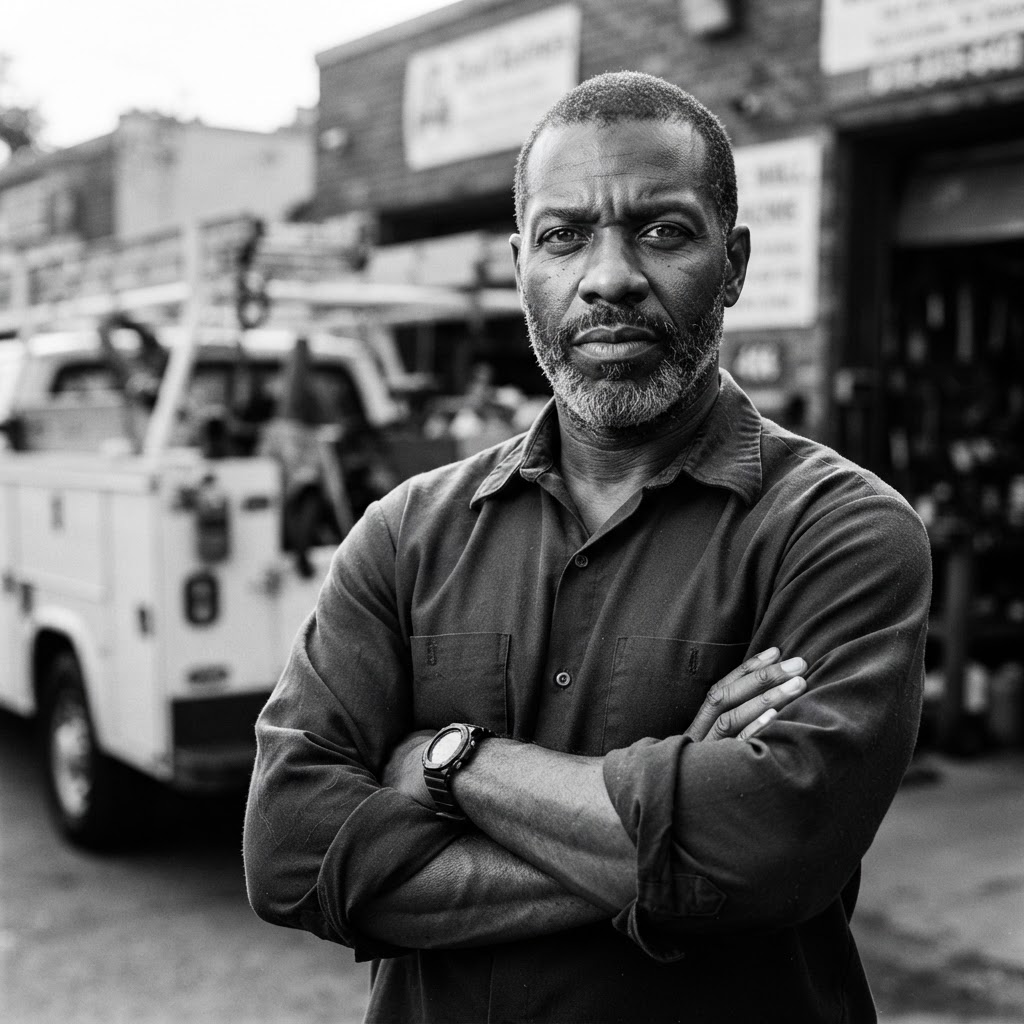

Marcus runs a small HVAC repair company outside Charlotte. Third week of July, his best commercial truck threw a rod and died on the highway — mid-job, mid-summer, during the busiest stretch of the year.

He needed a replacement truck fast. Not in six weeks. Not “sometime this quarter.” Now — because every day without that truck was a day of canceled jobs, angry customers, and lost revenue he couldn’t afford to lose.

So he did what most business owners do first. He called his bank.

They told him 45 to 90 days. Documents, underwriting, committee review, more documents. And even after all that waiting — there was no guarantee of a yes.

Marcus didn’t have 90 days. He had maybe a week before the damage to his business became permanent.

If that story sounds familiar, you’re not alone. Most of my clients have lived some version of it — an equipment breakdown, a slow season that dragged on too long, a big contract that needed materials up front. And every time, the bank’s answer is the same: wait.

And waiting isn’t free. Every day a contractor’s truck sits dead is a day of missed jobs. Every week a restaurant waits on a walk-in cooler repair is a week of spoiled inventory and turned-away customers. The bank’s timeline doesn’t care about your timeline. That’s the part nobody tells you going in.

Why Banks Move So Slow (And Why That’s Not an Accident)

Here’s the honest breakdown by funding type — so you know exactly what you’re up against before you waste weeks chasing an answer that might be “no” anyway.

Bank Loans: 45–90 Days (If You Qualify)

Traditional bank loans are the slowest option on the table. One to two weeks just to gather documents and submit. Two to four weeks for underwriting. Another one to two weeks for approval, legal paperwork, and funding.

Total: 45 to 90 days from application to cash in your account. And here’s the part banks don’t advertise — approval rates for small business loans sit below 30%. Most business owners go through that entire process, wait two to three months, and still walk away with a no.

SBA Loans: 60–90+ Days

Government-backed, better rates on paper — but the process is even slower than a standard bank loan. Figure 60 to 90 days minimum, and plenty of applicants end up waiting four to six months. You’ll need strong credit, real collateral, and a level of patience most growing businesses simply don’t have.

None of this is a knock on the people who work at banks. It’s just how the system is built. Banks are built for businesses that can afford to wait. If you can’t — and most small business owners can’t — you need a different path.

Revenue-Based Financing: 24–72 Hours

This is where speed stops being a luxury and becomes a real competitive advantage.

Application: 5 to 10 minutes. Document submission — usually just 3 to 4 months of business bank statements — same day. Underwriting and decision: 4 to 24 hours. Funding: same day or the next business day after approval.

Marcus applied on a Tuesday morning. He had the truck back on a job site by Thursday. No 90-day wait. No committee. No maybe.

How It Actually Works, Step By Step

- Step 1 — Apply. A short online application. No stacks of paperwork, no in-person meetings required.

- Step 2 — Submit statements. Just 3 to 4 months of business bank statements. That’s the core of what we review.

- Step 3 — Get a decision. Most applicants hear back within 4 to 24 hours — not weeks.

- Step 4 — Get funded. Same day or next business day after approval, deposited directly into your business account.

Repayment is built around your actual revenue, not a rigid fixed schedule that doesn’t care whether business is fast or slow that month. When revenue is strong, you pay more. When it slows down, your payment adjusts with it. That’s the entire idea behind revenue-based financing — capital that flexes with your business instead of working against it.

What Actually Slows the Process Down

- The one document most owners forget — incomplete or mismatched business bank statements are the #1 reason funding gets delayed, even with revenue-based financing.

- Deposits that don’t tell a clean story — wildly uneven monthly deposits make it harder to establish a fundable average, even for strong businesses.

- Recent legal or credit events — a recent bankruptcy or active judgment doesn’t automatically disqualify you, but it does require a closer look.

Fastest path to funding: have 3 to 4 months of clean business bank statements ready, apply with accurate information the first time, and respond quickly to any follow-up requests. That’s it. That’s the whole game.

The Honest Trade-Off Nobody Talks About

Speed costs something. Let’s not pretend otherwise.

Revenue-based financing is faster and far more accessible than a bank loan — but the cost of capital is higher than what a bank might theoretically offer you, if they said yes, if you waited three months, if everything lined up perfectly.

You’re paying for speed. You’re paying for flexibility. You’re paying for access that a bank simply won’t give a business like yours, on a timeline that actually matters.

When payroll is due Friday, when a truck breaks down mid-season, when a contract has a deadline that doesn’t care about your financing timeline — that trade-off is usually worth every dollar.

“But What If My Credit Isn’t Great?”

This is the question I hear more than any other, and it’s usually followed by business owners assuming they’re automatically disqualified. They’re not.

Revenue-based financing looks at your business’s actual cash flow — real deposits, real revenue, real performance — not just a credit score sitting in a file somewhere. A rough patch two years ago doesn’t define whether your business is fundable today.

“What If My Industry Is Considered Risky?”

Restaurants, trucking, salons, contractors, cannabis, healthcare — industries banks love to say no to, for reasons that have nothing to do with whether you actually run a good business. We work with business owners in exactly these industries every week. Your industry doesn’t disqualify you. Your revenue speaks for itself.

Real Numbers, No Fluff

Funding ranges from $10,000 to $500,000, depending on your monthly revenue and how long you’ve been in business. Most approvals land in 24 to 72 hours. Most funding happens same-day or next business day after that.

No stacks of paperwork. No sitting in a loan officer’s office explaining your business for the third time. No “let me check with underwriting and get back to you next month.”

Learn exactly how revenue-based financing works here — or skip straight to finding out what you qualify for right now.

Marcus didn’t lose his summer. His truck got fixed, his crew stayed on schedule, and his customers never knew there was a problem. That’s what fast, honest funding actually looks like when it works the way it’s supposed to.

If your bank has you sitting in a waiting room hoping for an answer that might never come, you don’t have to keep waiting. Takes two minutes. No credit check required to see what you qualify for.